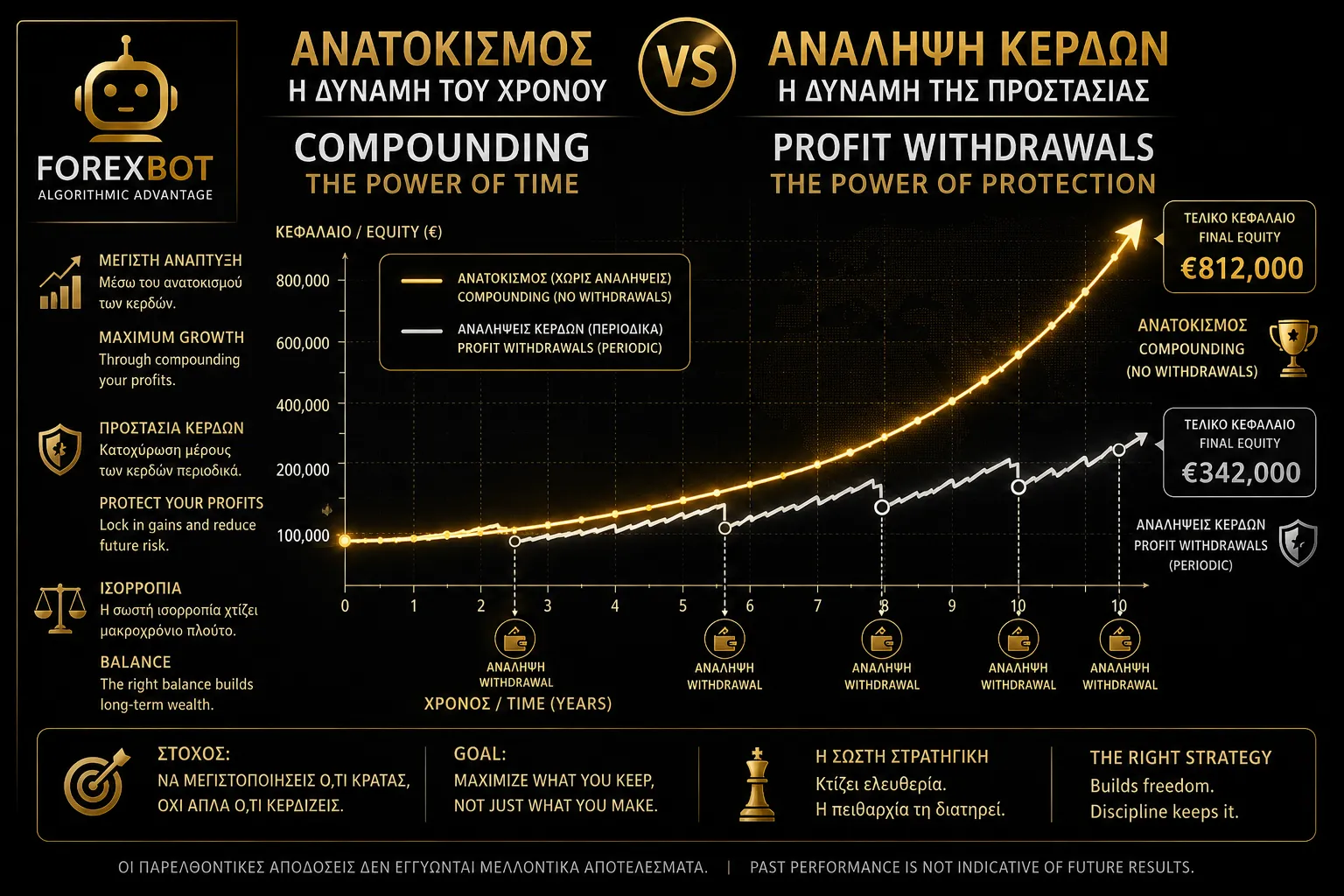

Compounding is often considered the most powerful force in capital management. When a strategy continuously reinvests its profits, each new trade is executed with slightly more capital and therefore has the potential to generate larger absolute returns. In theory, if a trading bot possesses a genuine statistical edge and its behavior remains unchanged for many years, fully reinvesting profits produces the highest possible capital growth. Mathematically, this is the optimal solution.

In reality, however, markets are not static. Liquidity changes, spreads evolve, market participants adapt, and the conditions that created a historical edge may weaken over time. Even strategies that have survived financial crises, periods of extreme volatility, and multiple economic cycles cannot guarantee that the future will perfectly resemble the past.

This creates an interesting dilemma. As capital grows through compounding, the absolute value of every future drawdown also increases. A system with a historical maximum drawdown of 15% may lose €1,500 on a €10,000 account, but the exact same percentage represents €10,000 when the account has grown to €70,000. The risk percentage remains unchanged, yet the financial and psychological impact becomes significantly larger.

For this reason, many professional investors choose to withdraw profits periodically. One common approach is to secure part of the profits at the end of each year. This allows the strategy to continue growing while converting a portion of the returns into real, protected capital outside the trading account. Another popular method is to withdraw profits whenever the equity curve reaches a new All Time High. In this case, a percentage of the newly generated gains is removed from the system and protected from future periods of underperformance.

The disadvantage of withdrawals is obvious. Every euro removed from the account no longer participates in the compounding process. As a result, the long-term growth rate of capital decreases. An investor who never withdraws profits will theoretically end up with more capital than one who systematically secures part of their gains.

The real question, however, is not which option produces the highest theoretical return. The real question is which option better serves the investor's objectives. If the goal is maximum growth and there is complete confidence in the long-term durability of the strategy, then full compounding is the logical choice. If the goal is gradually transforming returns into lasting wealth, then periodic profit withdrawals may represent a more balanced approach.

Ultimately, there is no universally correct answer. Compounding maximizes capital growth, while withdrawals maximize the protection of already-earned profits. The optimal balance is often found somewhere in between, allowing the strategy to continue growing without leaving its entire historical profit exposed to future uncertainty.