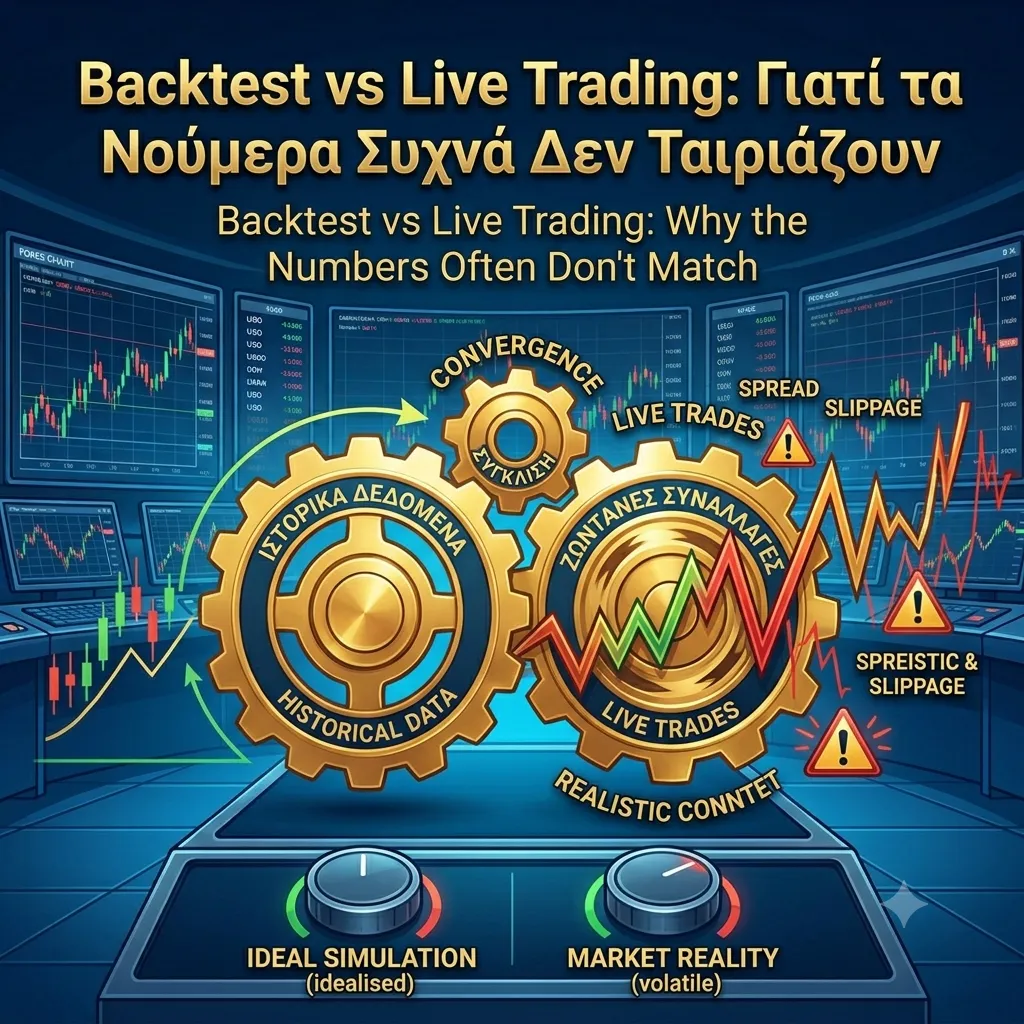

A backtest is testing a strategy on historical data: "if I had run these rules over the past 15 years, what would have happened?". Live trading is applying the same rules in real time, with real money.

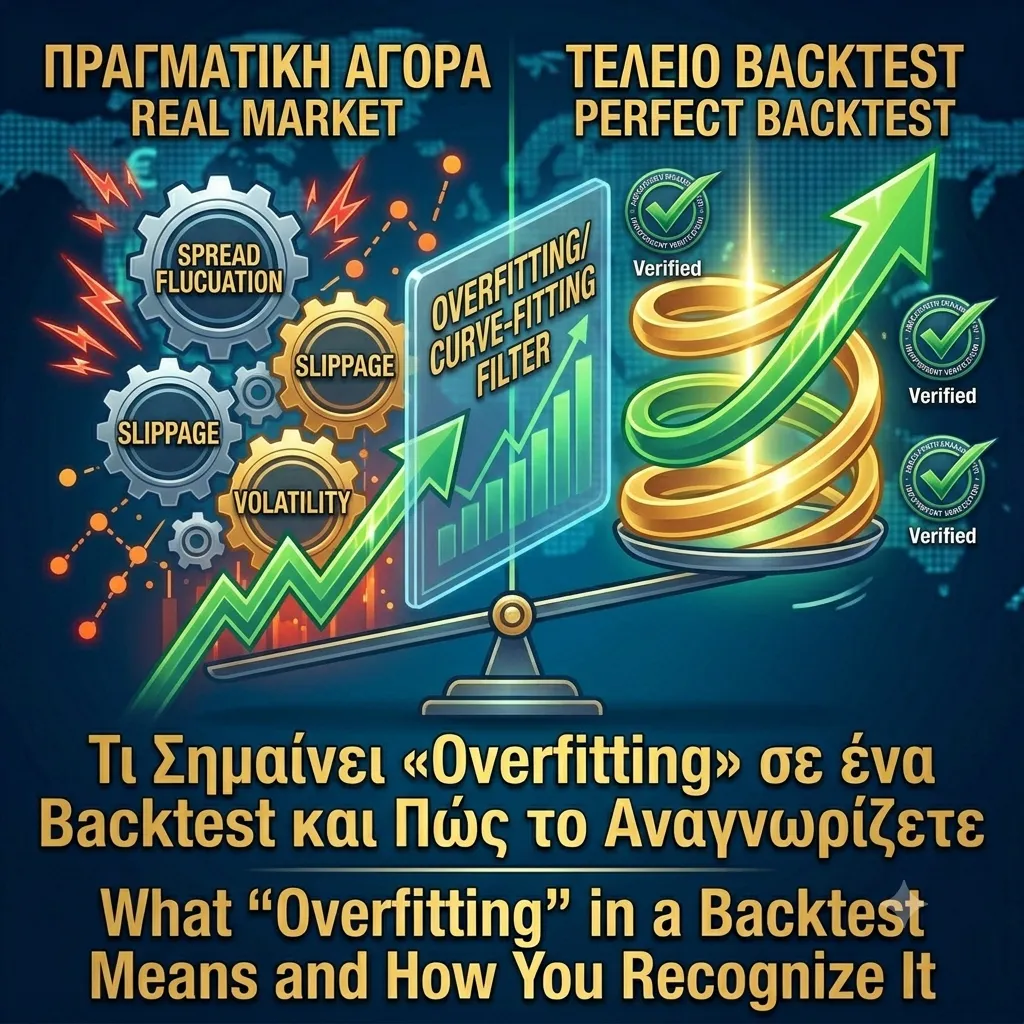

The problem: an impressive backtest is extremely easy to manufacture. You can "tune" the rules until they fit the past perfectly. The result looks wonderful on a chart — and collapses on day one in a real market.

In real execution, factors appear that the backtest often ignores: the spread widening during news, slippage (the price you get differs from the one you asked for), execution delay, price gaps over the weekend.

That is why the most important — and hardest — property of a system is not its backtest performance. It is convergence: how closely real performance tracks what the historical simulation predicted.

When the live trading curve statistically follows the backtest's behavior over a meaningful sample of trades, the probability that the edge is genuine — and not a product of overfitting to the past — increases significantly. That is the number you should ask to see, not the prettiest backtest.