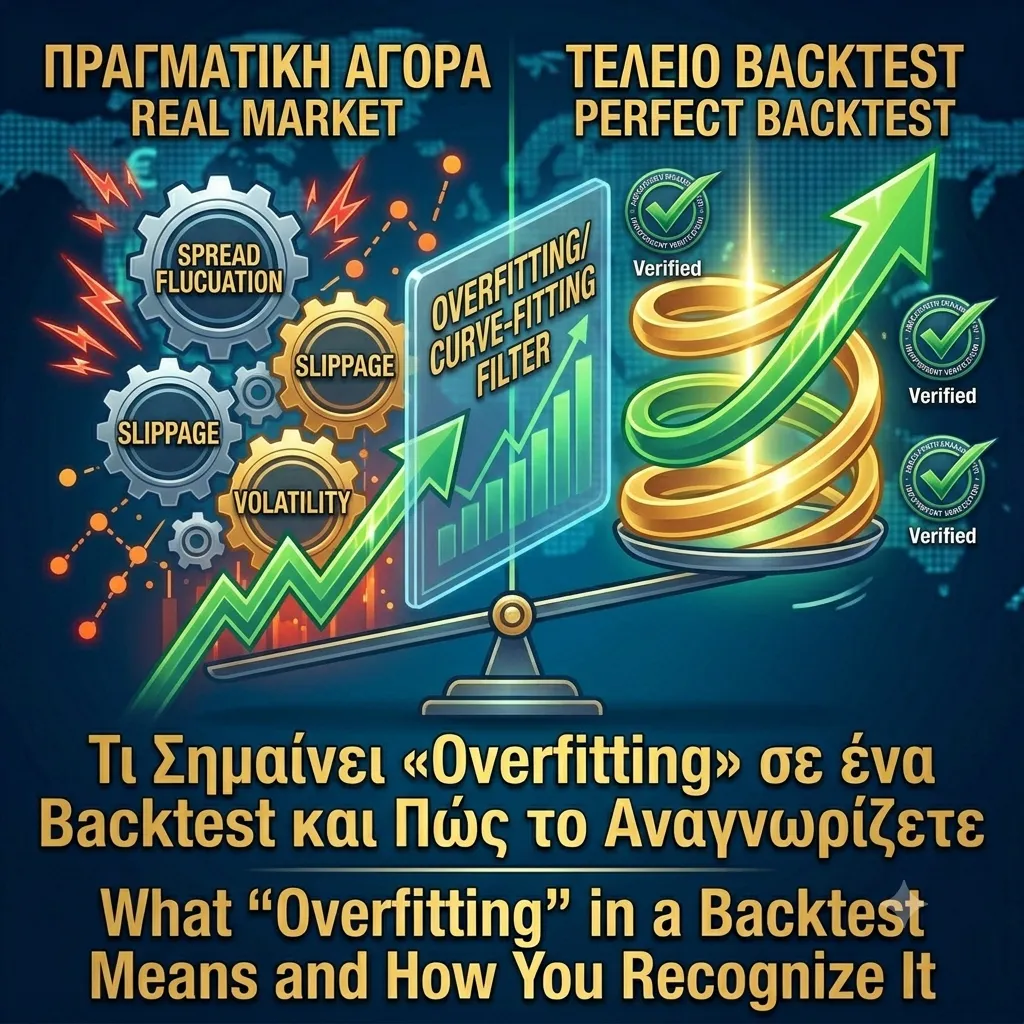

Overfitting (or curve-fitting) is when a strategy has been adapted so much to historical data that it has essentially "memorized" it instead of learning a real pattern. The result: a perfect backtest, but failure in the real market.

Think of a student who memorizes the answers to old exams instead of understanding the material. On the same questions they get top marks. On new ones, they collapse. Overfitting is exactly that, in strategy form.

How does it happen? The creator adds more and more rules and "tweaks" parameters until the backtest curve becomes impressive. Each extra adjustment makes the chart prettier — and the system more fragile in the real world.

How do you spot it? First sign: too many rules or parameters for each currency. If every pair has its own "magic" settings, it's probably adapted to the past.

Second sign: performance collapses outside the test sample. Reliable creators test on data not used in development (out-of-sample).

Third and most important: the backtest–live gap. If the system is overfitted, live trading will quickly diverge from the backtest. Conversely, the convergence of the two over a large sample is the best proof that the edge is genuine and not memorization.