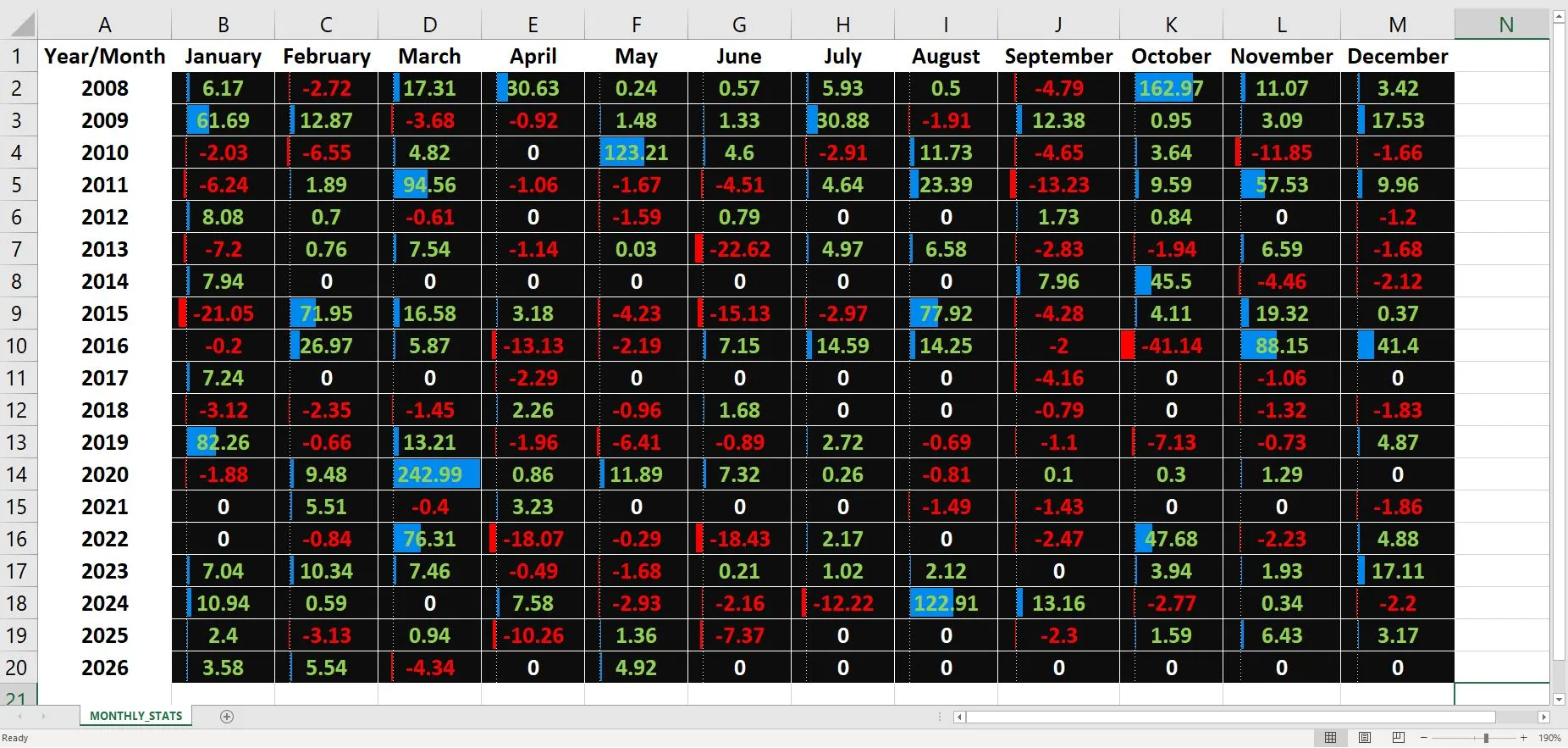

At first glance, the choice seems obvious: a system returning +80% per year is better than one returning +15%. But this thinking ignores the critical half of the equation: risk.

Imagine two versions of the same strategy. The first targets +80% per year, but with a maximum drawdown of 57% — meaning at some point the account could lose more than half of itself before recovering. The second targets +15%, with a drawdown of just 9%.

Which is "better"? It depends entirely on you. The first requires enormous psychological endurance and capital you can afford to watch shrink. The second is far smoother, but with lower returns.

The beginner's mistake: they choose the high return, feel strong in the good periods, and then abandon ship in panic at the first big drawdown — locking in the loss. In practice, they make less than they would have with the "boring" version they could have held onto.

That is why a serious approach doesn't offer "a" number, but different risk profiles of the same strategy. The goal is not maximum profit — it is matching the risk to your personal tolerance, so that you stay in the game.